What's the long-term difference between 7% and 14% CAGR in retirement?

Apr 02, 2025

VTS Community,

Great question from a member I thought others may be interested in:

"How much of a difference does it make after 30 years if an investor doubled their rate of return?"

I like going over the numbers with questions like this because the truth is, very few investors actually do play around with retirement fund calculators and many people just haven't seen the numbers.

People may assume that getting double the rate of return will roughly translate to twice as much money in retirement right? I suppose that makes some sense, but even if they assume there must be an exponential compounding element they may not know how significant it actually is.

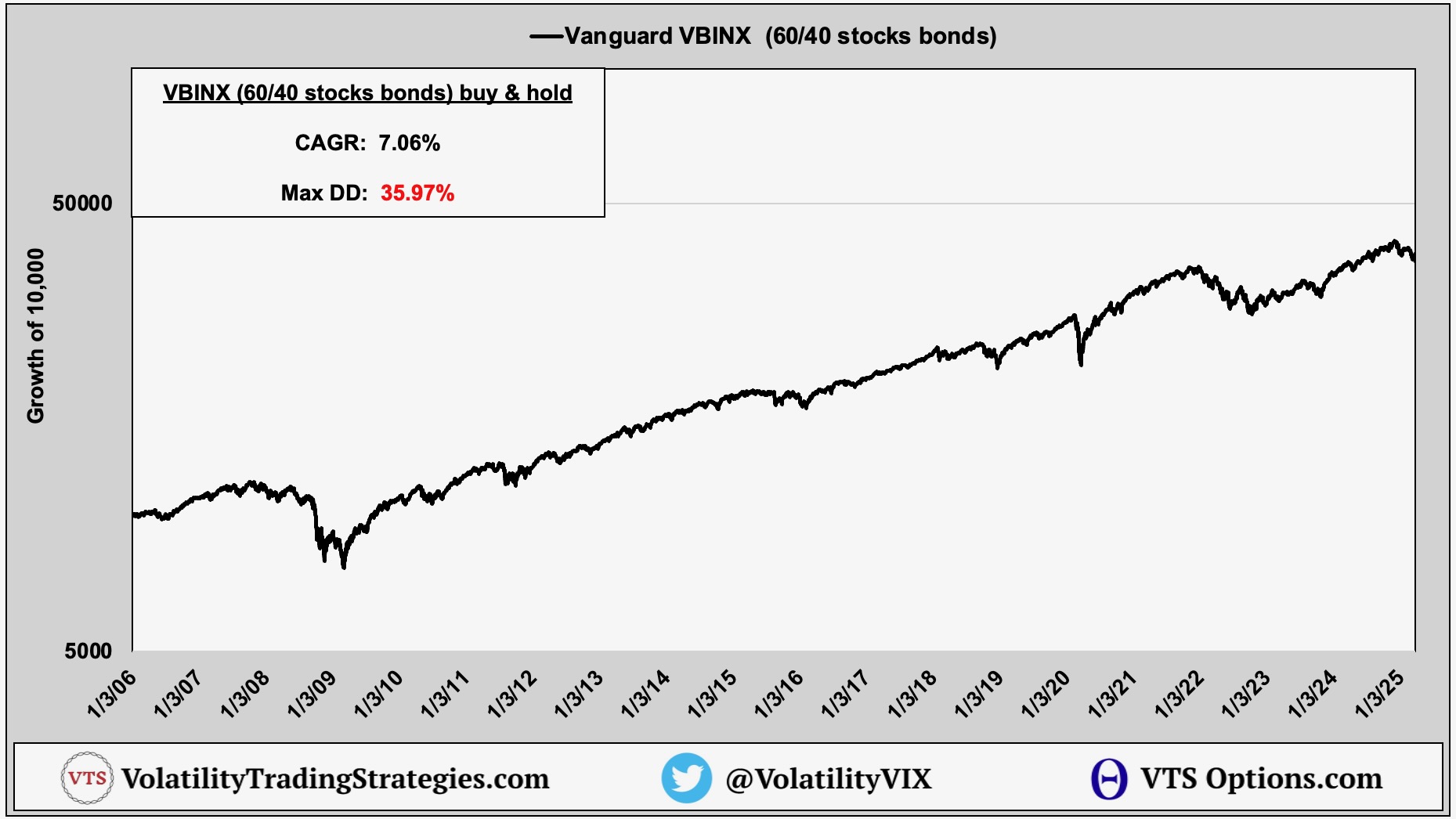

To establish a baseline rate of return we will use the trusty old Vanguard VBINX, a 60% stocks 40% bonds balanced index fund.

VBINX in the last 20 years:

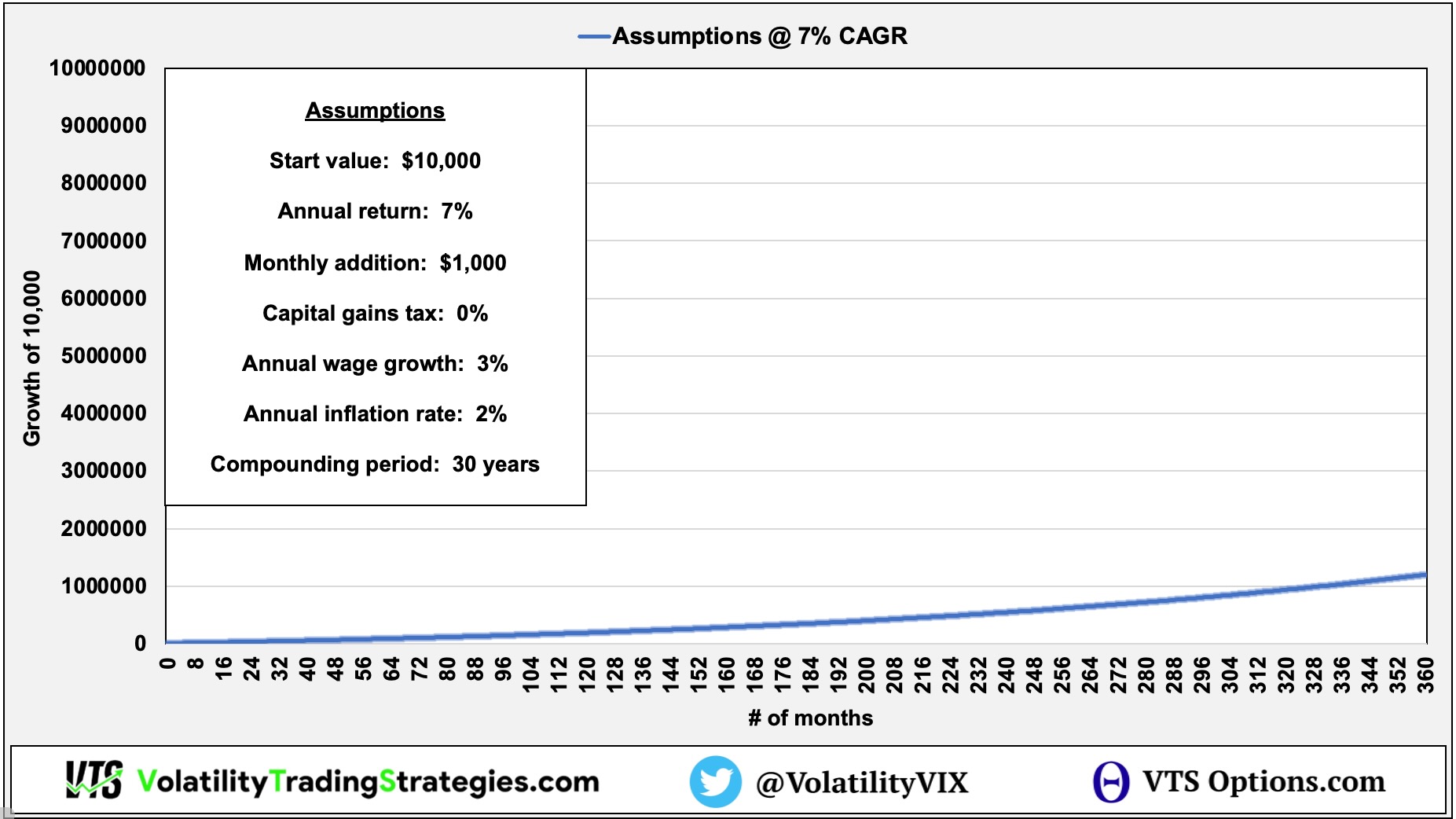

Using the baseline VBINX we can now establish some baseline assumptions for our test to see what the retirement value is:

Start Value: $10,000

Annual return: 7%

Monthly addition: $1,000 + wage growth

Capital gains tax (assume tax deferred): 0%

Annual wage growth: 3%

Annual inflation rate: 2%

Compounding period: 30 years

It may surprise some people to see that starting with $10,000 and adding a little every month turns into just shy of 1.2 million dollars in retirement. The key variables here are time, rate of return, and money added. Seeing the numbers, pretty much anybody can be a millionaire in retirement right?

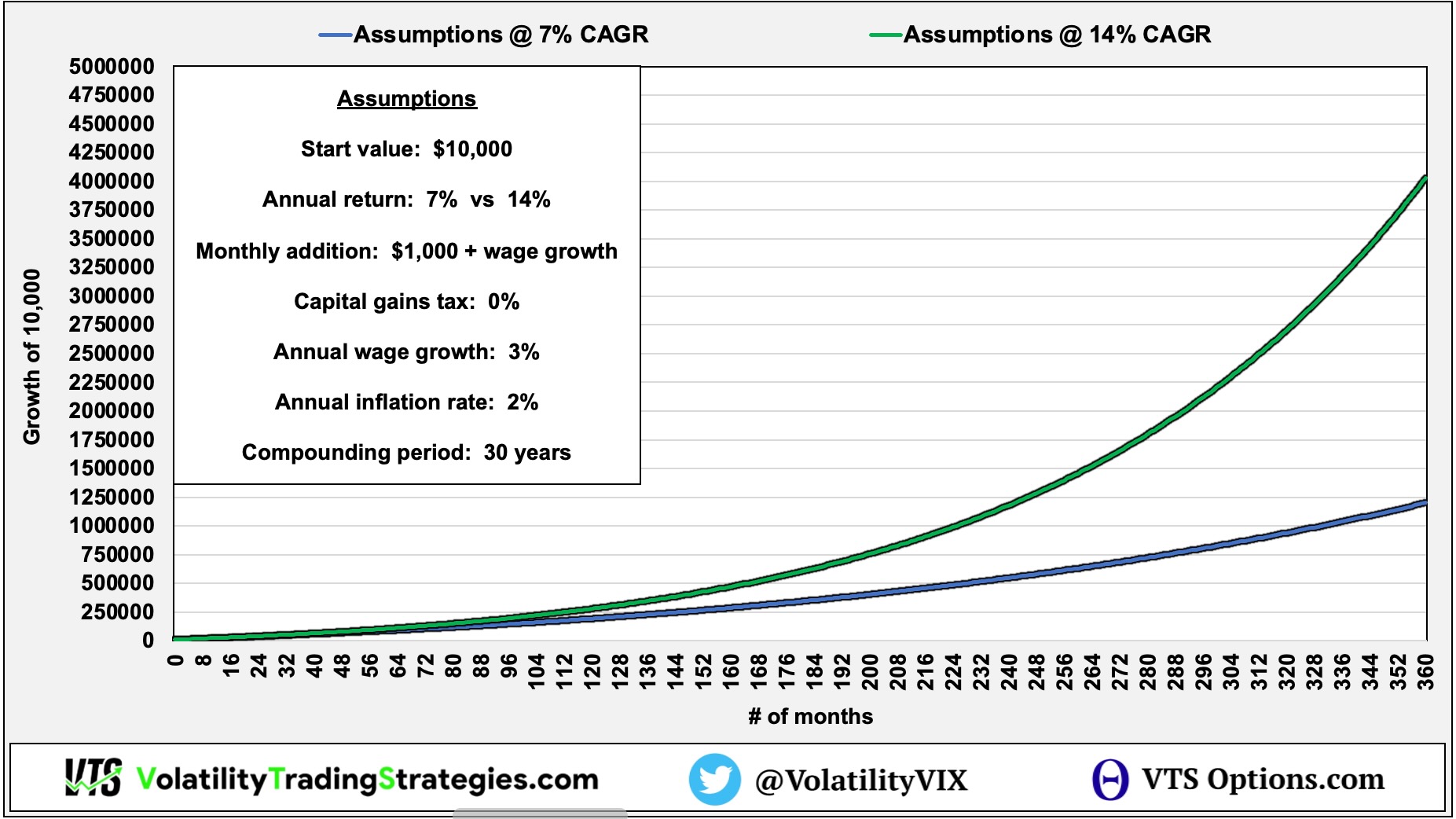

So what happens if that investor doubles their rate of return?

Using the same assumptions but now they get 14% a year instead of 7%:

Now we can see the exponential power of compounding!

Starting with a very modest $10,000 and adding what I would say is an achievable amount of $1,000, this investor after 30 years is a multi-millionaire and sitting on over 4 million dollars.

Patience and consistency is the whole game

Seeing the numbers and how truly achievable it is to become a multi-millionaire in retirement, that does beg the question: Why doesn't everybody achieve this? I'd actually like to unpack some of the reasons in an extended livestream in the future so I'll keep this short.

1) They start investing late. If you want to hit your goal at 65 years old that means you have to start at 35. How many people can really say they started saving $1,000 a month at age 35? I think most people could if they put their mind to it, but do they?

2) They don't trust the long-term process. Most people pull the plug on an investment strategy at the first sign of trouble, or after the first bad year. I've seen this first hand. My parents probably had half a dozen financial advisors over their investing time horizon, and they would bounce around every time the performance lagged. Now this isn't an advertisement to stick with an advisor. If you're not getting at least a baseline level of growth you leave. The point is though, 30 years is a VERY long time, and it requires patience and consistency to hit your goal.

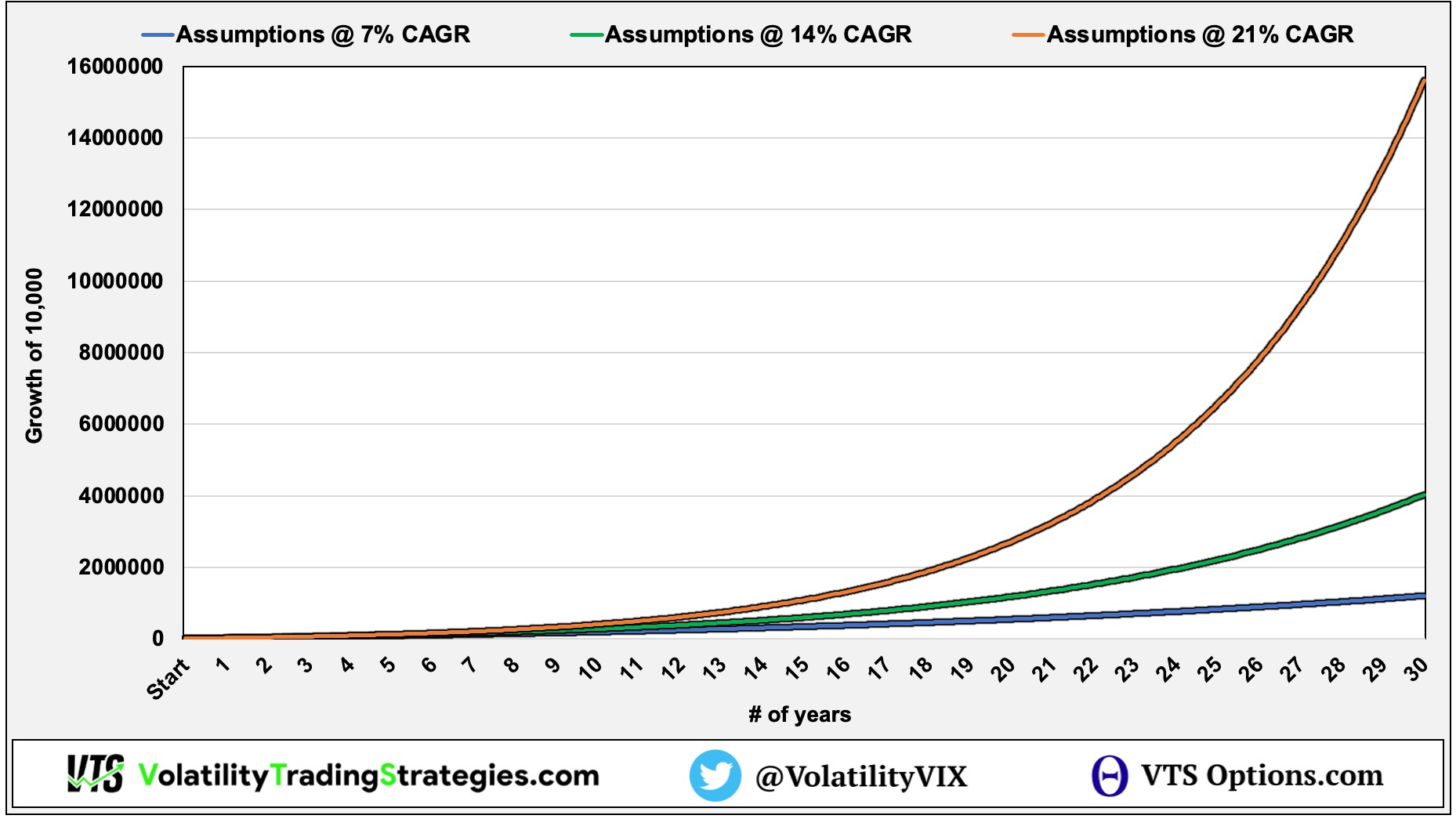

Want me to really blow your mind?

What if an investor tripled the VBINX and actually got a 21% annual return? (like I have with my VTS Strategies in the last 13+ years)

It starts quite slow, takes 15+ years to really get that compounding working in your favour, but the parabolic nature of compounding over time can be pretty amazing.

If an investor did manage a 21% annual return for 30 years, even with a very modest addition of $1,000 a month they will be sitting on 16 million dollars in retirement.

Will VTS average 20% a year for another 20 years? Honestly, I have no clue. That is my goal and I do have confidence, but only time will tell on that one. What I can say though is, even if I fall short of my goal and actually end up with something around 15%, that is enough to make anyone a multi-millionaire if they stay the course. Just sayin' :)

Take Control of your Financial Future!

Profitable strategies, professional risk management, and a fantastic community atmosphere of traders from around the world.